Italy: O sole mio!

Or how the narrative around Italy's dependence on natural gas might not be giving enough credit to the country's progress in its installed solar capacity.

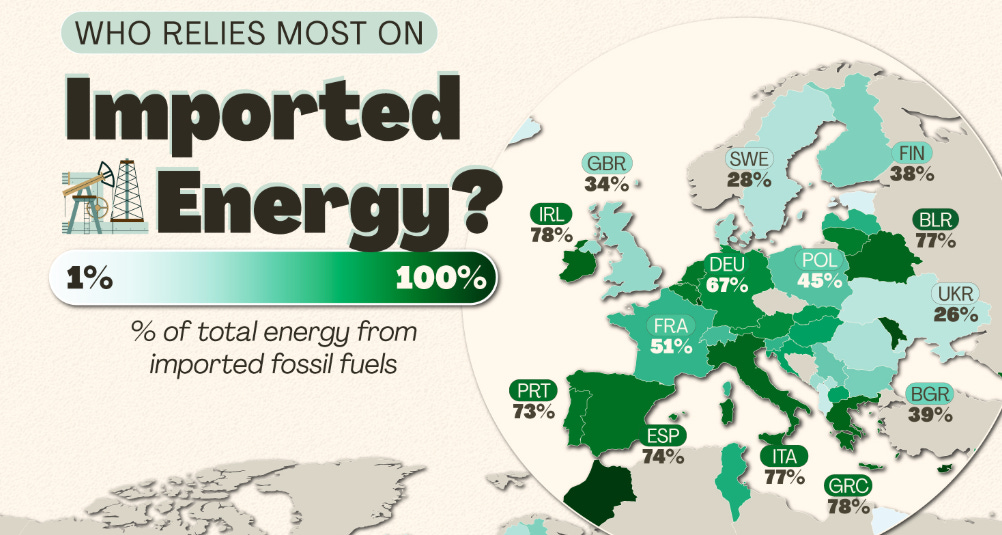

For those working in the energy field, Italy might be known for something more than the mountain of tourist clichés which I won’t even bother enumerating here: its heavy reliance on imported fossil fuels. Looking at data, latest stats from 2025 report that 77% of the country’s energy use comes from imported fossil fuels . That might seem a lot, until you realise that many European countries are not doing much better, given that it’s the stuff needed to run most of our transport system and industry (for now), and that no European country is a major oil and gas producer anymore.

In this article I therefore wanted to take you on a bit more unconventional tour of Italy to untangle the facts regarding Italy’s dependency on fossil fuels, and particularly natural gas. After all, we are talking about the EU’s third largest econmy by GDP, with a population larger than all of the Nordics and Benelux combined. Knowing that, it seems pretty important to have a better vision of the energy reality which the country is confronted with.

To be clear: Italy’s dependence on (and therefore vulnerability to) natural gas imports is undeniable, whether it is to power its gas power plants or keep its manufacturing power house running. Italy’s manufacturing output is the 8th largest in the world (depending on the chosen metrics), ahead of countries like France and the UK, with fashion and the automotive industry playing an important role (I said I would try to stay clear from clichés, but I suppose there is often some truth to them). Italy is also producing high-quality machinery used worldwide by the manufacturing sector itself (funnily enough). All these sectors often require energy-intensive industrial processes, with very high temperatures difficult to achieve without burning fossil fuels. All these industrial applications are often what is called “hard to abate” sectors in the energy jargon, meaning that replacing the use of fossil fuels in their applications is not straightforward, although electrification is giving increasing hopes on that front as well (cf. the excellent paper by Madeddu et al. on the topic).

On the power production side, natural gas-fired power plants represented 45% of the country’s electricity mix in 2021, one of the highest shares in Europe. One can wonder how Italy came about to make this choice for its electricity mix, considering that the country barely produces any natural gas itself.

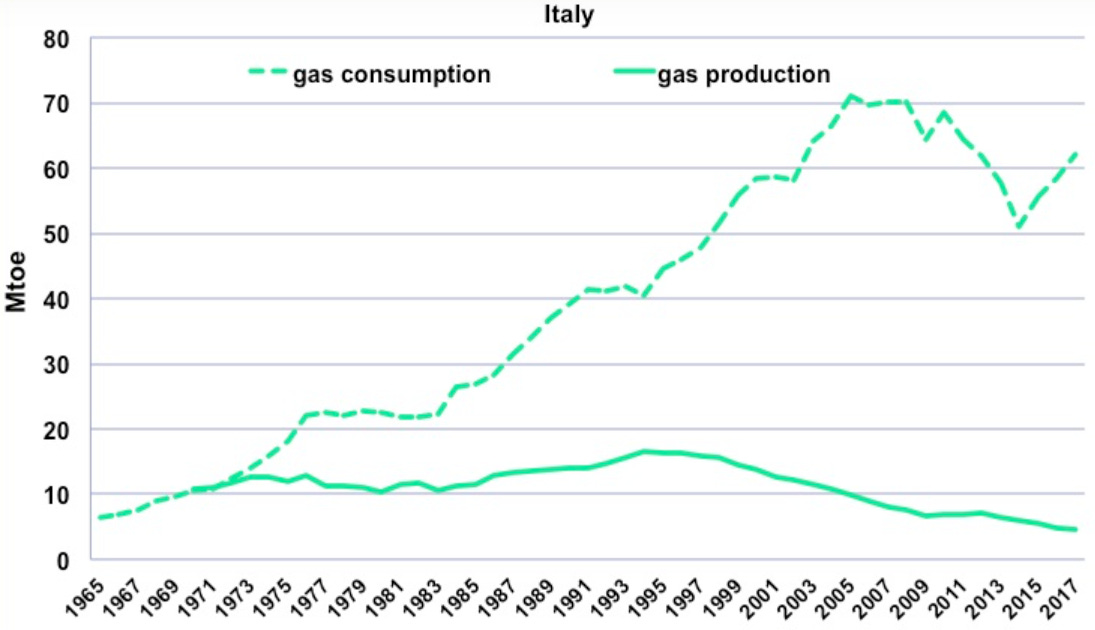

The reliance on gas as a source of electricity has historical roots. The discovery of gas in the Po Valley in the 40s came at a time where the entire country’s economy needed to be kick-started again after the Second World War. By 1960, Italy was even the largest gas producer and consumer in Europe. This early enthusiasm for this convenient domestic energy source, located close to its industrial consumers in the North, quickly locked in natural gas as an essential ressource for the country’s economy (but not yet for the electricity sector at this point). As consumption grew, imports and the corresponding buildout of pipelines became the inevitable next step.

Following the oil shocks of the 70s and the favourable alignment of factors pushing for natural gas (development of more efficient combined cycle gas turbines, privatisation of energy producers in the 90s leading to investments in these more profitable power plants, phase out of nuclear power in 1987, increasing environmental pressures), gas also started to make its way in the electricity sector by replacing oil-fired power plants. With gas pipeline infrastructure already in place, the transition to gas in the power sector was a low-hanging fruit. Natural gas has since played a key role in the country’s electricity mix.

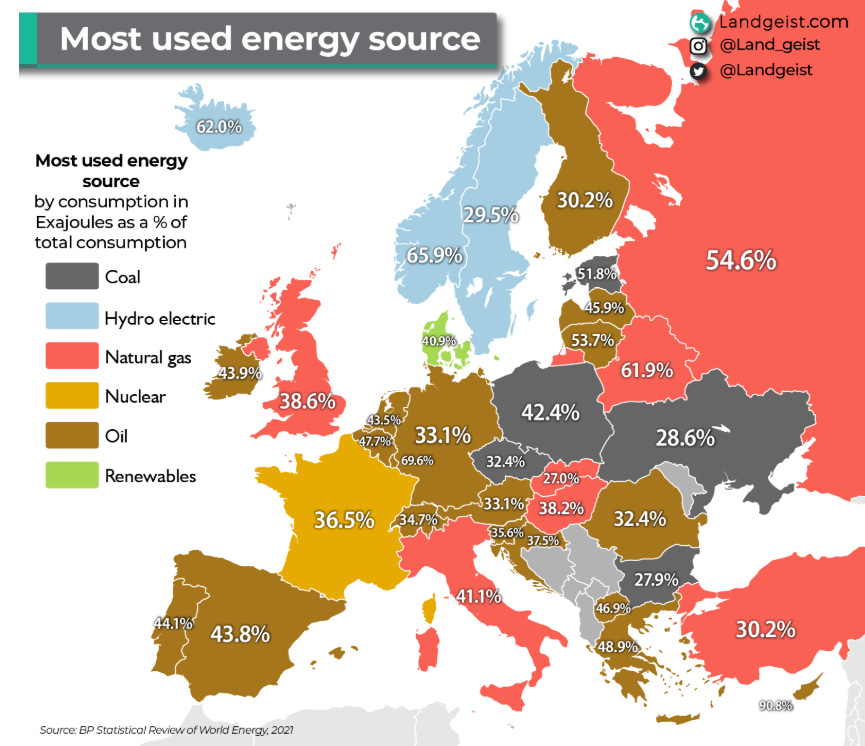

The fascinating map below shows the extent to which this dependency on gas has become characteristic of Italy. In fact, only Russia and Belarus have a higher dependency on natural gas as energy source, the former being a major producer and the latter being completely dependent on the former. While it may seem that Italy’s situation is not much worse than the UK’s, let’s not forget that the UK’s domestic gas production still represented 50% of the country’s total consumption in 2024, although this number has been falling rapidly over the last decades. After a short-lived peak production in the 90s, Italy currently only covers 4.2% of its total gas consumption from domestic production.

Key takeaway 1: Natural gas came to play a key role in Italy's manufacturing sector, and eventually its power sector, kickstarted by a post-war consumption based on domestic production, and quickly replaced by imports supported by an extensive gas pipeline infrastructure.

This high dependence on imported natural gas is where the trouble begins. Before the beginning of the Russian invasion of Ukraine, Italy imported 40% of its natural gas from Russia. As gas prices started to increase by the end of 2021 and led to the energy crisis of 2021-2023 through a combination of factors (high demand after post-COVID recovery, cut-off of Russian gas supply routes following European sanctions, drought in the summer of 2022 compromising the cooling system of coal and nuclear power plants and reducing the output from hydropower, maintenance of French nuclear due to corrosion issues, etc.), Italy’s addiction to natural gas particularly made the news. In August 2022, power prices on the wholesale market shot up to €543/MWh , driven by the factors mentioned above, whereas electricity prices previously rarely had averaged over €80/MWh. Prices have fortunately cooled down quite a bit since, but remain almost consistently above the €100/MWh mark, which is enough to make it a heated political topic.

Looking on the political front, Prime Minister Giorgia Meloni’s agenda does not seem ready to back down on natural gas. A sample of recent news state for example that Meloni plans to make Italy a “gas hub” in the Italian region and that her government continues to see a key role for gas in the country’s energy mix, with the National Energy Climate Plan representing a major setback for renewables. In general, the government does seems to have no plan to phase out gas, and on the contrary seems to double down on it.

Key takeaway 2: Despite the detrimental impact of the country's gas dependency on it's economy, particularly shown by the recent energy crisis, Italy's current government does not seem ready to back down on gas.

So far, everything I wrote, backed by data, seems to confirm Italy’s gas dependency. Yet this is where having up-to-date data is essential to draw conclusions on the direction the country is taking, particularly in the energy field. You might have noticed that no data I gave you so far is more recent than 2022. Yet it turns out this marks a critical turning point in most European countries’ energy policies. This was made clear on a political level through the introduction of large energy support packages such as RepowerEU on a European level and equivalent measures on national levels.

Even in Italy, despite the seemingly unfavourable political climate, major support mechanisms for efficiency and renewable energy have been put in place. Following FER 1, a Ministerial decree from 2019 supporting solar, wind, and hydro renewables, FER 2 was passed in Italy in 2024 to support non-mature technologies such as floating solar, offshore wind, geothermal, etc. through 20-year contracts, providing visibility for investors. A plethora of other initiatives have also been put in place, such as support mechanisms for agricultural PV (Decree N. 436) in 2023, for self-consumption (Decree N. 414) in 2024, for energy efficiency investments (Transizione 5.0 Decree) in 2024. Most of these iniatives focus on providing investment security by ensuring long-term fixed tariffs called Feed-in-tariffs.

The challenge of course is to ensure that the state, and therefore the taxpayer, does not get ruined from these support mechanisms. Previous support mechanisms such as the Conto Energia support mechanism for solar PV, which ran from 2005 to 2013 and successfully spawned a first wave of solar capacity installations, was eventually phased out after increasing complaints about its cost. As already mentioned in previous posts, solar PV has however experienced drastic cost reductions since then, allowing it to be competitive on electricity markets without subsidies. However, the revenues from electricity markets can be extremely volatile, which can make many investors go cold. The main benefit of such fixed feed-in-tariffs from the state is therefore not necessarily to financially support an industry which is already mature enough as it is, but rather to provide long-term visibility to investors.

To what extent these policies are and will be successful is too early to say, but looking at more recent data from the IEA, it seems that renewable project developers in Italy have not been waiting too long to make things move.

Several interesting observations can be made:

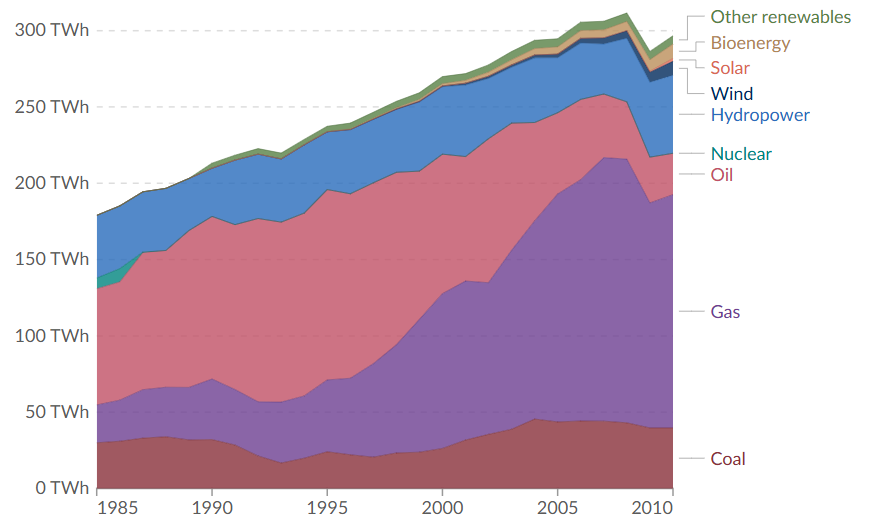

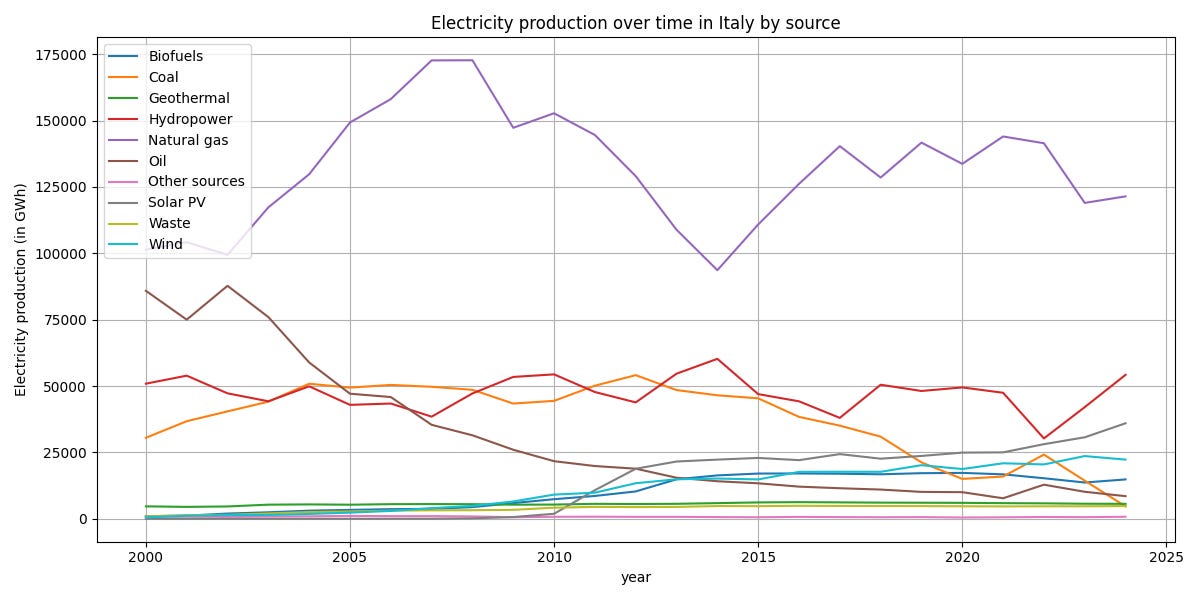

Firstly, the grey line corresponding to solar PV production is showing signs of revival over the past three years, after a first increase from 2010 to 2013, which corresponded to the period of the first Conto Energia support mechanism. On a yearly resolution, such an increase is largely due to additional capacity installation.

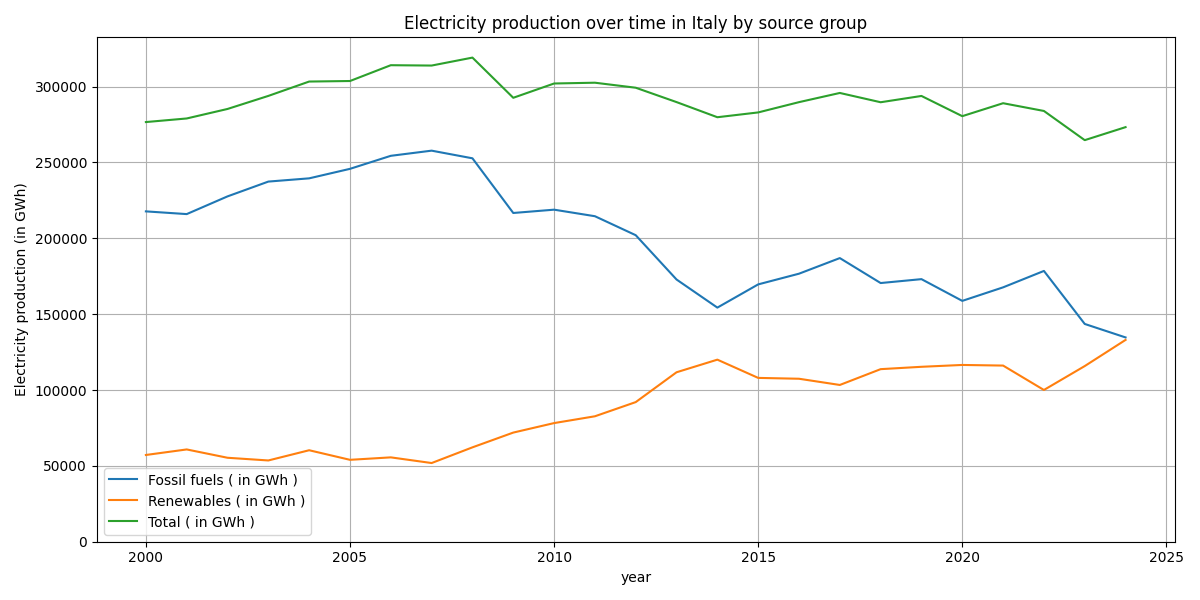

Secondly, the orange line corresponding to coal production has been steadily decreasing since 2012. Comparing values between 2012 and 2024, the output from natural gas and hydropower has barely moved, yet coal production has all but disappeared. While Italy’s total electricity consumption has slightly decreased over that timespan, the majority of the answer is to be found in the aggregation of solar PV and wind, which have seen a considerable increase over that timespan.

If renewables continue on their current trend and coal has reached near 0 production, it very much seems like gas is next in line to be displaced from the country’s electricity production stack. Fresh numbers for 2025 in a few weeks should help to confirm this trend or not.

Taking all of these dynamics into account, Italy achieved a symbolic yet by no means insignificant milestone in 2024: for the first time, renewable sources (hydro, solar, wind, biofuels, and geothermal) reached 50% of the country’s total electricity production.

More importantly, it seems that the nearly perfectly parallel evolution of total electricity production and fossil-based production since WWII in Italy has met a definitive end in 2008, with the gradual uptake of renewables. After a 10-year plateau until 2022, a renewed uptake is observed in recent years. Although part of this can be attributed to good hydrological years, it is undeniable that particularly solar is experiencing a renewed uptake.

Finally, significant achievements can also be mentioned on the consumption front. In 2022, Italy even outperformed the 15% gas consumption reduction target set by the EU, achieving a 18.6% reduction. Naysayers will point at demand destruction caused by the energy crisis, but numbers show that Italian industry’s energy efficiency has been continuously improving, to achieve a 25% reduction in energy consumption in 2022 compared to 2000, for a given amount of industrial output. Italy’s National Energy Climate Plan of 2024 also includes a significant increase in building renovation rate and heat pump installations.

Key takeaway 3: solar capacity installations have taken up speed again in recent years, after a few years of lull. The high power prices, combined with a drop in solar PV prices, seem to have created a favourable context. Recent energy policies seem to support these developments, despite the pro-gas declarations made by the Meloni government.

Final remarks: Despite political backlash against renewables (in appearance) and a deep dependence on natural gas, Italy’s energy transition shows signs of taking up speed in recent years. Contrary to the impressions which public declarations of politicans seem to give, growth of renewable capacity and energy efficiency improvements are backed both by encouraging incentives and favourable market conditions.

Whether these drivers are enough to continue this trend in the years to come will be interesting to follow. In the electricity sector in particular, as other fossil fuel sources have already been pushed out by renewables, the question is whether gas will have the same fate. While favourable renewable investment conditions can carry this some of the way, nationally planned energy policies supporting renewables are necessary to achieve a renewables-dominated electricity system, not least of which a major upgrade of the grid, which is a particular sensitive topic, given the country’s North-South geography. For example, the grid would have to be reinforced enough to transport electricity generated from solar PV in the South to industrial consumers in the North. Additionally, electrifying these industrial consumers to make them able to consume the additional power from renewable sources will be no easy task, and would therefore benefit from energy policies favourable to electrification investments.

With Giorgia Meloni’s government in power, direct political support at a national level does not seem promising. However, the solar PV industry could indirectly be aligned with politicans political agenda, by supporting local industries and jobs. Indeed, Italian companies like 3SUN are expanding their solar manufacturing capacity in Italy, producing innovative high-efficiency solar panels. Their gigafactory in Catania (Sicily) is the largest solar industrial facility in Europe, with a current production capacity of 1.8GW/year (corresponding to approximatly 3 million solar panels) and expected to scale up to 3 GW.

As long as the solar market is developing, these industries might do fine on their own. But, like any industry, they will also need political support, or at least no political opposition, as soon as they are facing more difficult times.

While gas has carried Italy a long way over the last decades, it seems that renewables, and particular solar, are bringing a wind of change to the country. This could benefit the country both economically, geopolitically, and last but not least, environmentally. The biggest challenge for Italy will be to accept and embrace this change. It makes one wonder whether the time has not come for fossil fuels and their promoters to end up, like all other fossils, in a museum, in order to allow the country to move forward.

I would like to thank my colleague Francesco Colaci for the interesting discussions which inspired this post. It always helps to have a local insight to give a bit more context to the analyses.